A sweltering summer has once again highlighted the chinks that exist in India’s power sector. While the economy was gradually recovering from the pandemic hit, higher than normal daytime temperatures in April sent power demand soaring. As per the Central Electricity Authority (CEA) data, power demand in April was higher by 13.7% year-on-year (YoY) despite a high base (39% YoY growth in Apr-21).

As supply could not keep pace, it led to a six-year high deficit. As a result, not for the first time though, did we see spot power prices jump sharply. But never did we see the day ahead exchange prices stuck at ?12 per unit for days together. It could have been even higher but for the regulatory cap imposed by the CERC.

What led to this situation

We have heard the reasons before; the shortage of coal reserves across multiple power plants. At last count, there were around one hundred units, which had less than the normative level of coal stocks.

Either these units were not getting enough supplies from Coal India for reasons of delayed payments or lack of adequate railway rakes to transport the coal. Power plants running on imported coal were also running at low PLFs due to the sharply higher global prices. What has further accentuated the crises this time around is the high natural gas prices, which forced several gas-based utilities to shut their units.

As if this was not enough, the Russian-Ukraine war started. It could not have happened at a worse time. Just when the western world economies were starting to recover from the pandemic, energy demand rose more than expected.

However, Russia played spoilsport by not increasing supply to Europe because of which storage levels fell. It was considered a pressure tactic for the EU to allow gas to flow through the Nord Stream II pipeline (connecting Russia to Germany). However, the EU regulators decided to withhold permission for the Nord Stream II pipeline to start on grounds of competition.

All this only led to a sharp increase in gas prices in the EU. After Russia invaded Ukraine, the situation worsened with the former cutting off gas supplies to Bulgaria and Poland for their refusal to pay in Rubles. We have not heard the last on this and no one knows what will happen next.

Post the start of the war, crude oil prices also gained strength with the OPEC adamant about not increasing production to compensate for the expected drop in supplies from Russia. So, it was only natural for other energy sources like coal to take the lead and firm up.

With the EU not able to shrug off its dependence on Russian natural gas, but intent on responding to Russian aggression, they did the next best thing possible. They announced a blanket ban on the imports of Russian coal from August 2022 onwards. This proposal will severely hit the supply of thermal coal given that the EU imported 68% of its requirement of 44.2 Mn MT from the country in 2021.

What makes the situation even more worrisome is the decision by Japan and South Korea to follow suit. Both Japan and South Korea imported 30-35 Mn MT of thermal coal from Russia in 2021. So, what will replace Russian coal for these countries?

Given that Russian coal is of a higher grade, the demand can shift to the USA, Australia, Colombia, and South Africa. However, the choice is not so simple. For the EU, importing from Australia and South Africa will mean higher logistics costs.

The same is true for Japan and South Korea if they buy more from the USA and Colombia. But there are other worries as well. The South African logistics network is grossly inefficient and exports from the Richard Bay terminal in Durban are much lower than the stated capacity of 100 Mn MT per annum. In 2021, the terminal exported 58.7 Mn MT – the lowest volume since 1997.

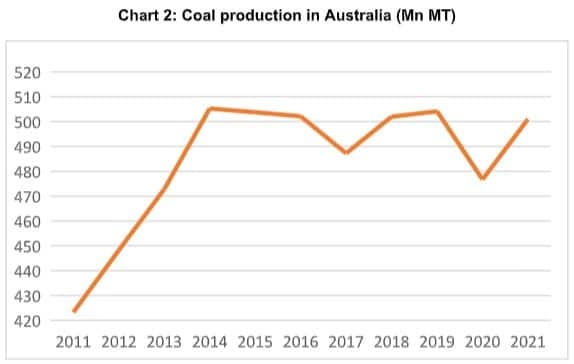

On the other hand, Australian coal production has stagnated at around 500 Mn MT since 2014. We are not considering Indonesia in this analysis as the coal it produces is of a lower grade.

The other side of the argument is that the two largest coal importers in the world viz. China and India will opt for Russian coal thereby reducing demand for Australian and South African coal. But here also it is not as simple as it sounds. Buying more from Russia will increase the logistics cost.

Secondly, till the sanctions are in place on the Russian financial system, it will be difficult for users especially those with a global presence to trade with Russia. For instance, Tata Steel announced that it will not buy coal from Russia, which accounts for around 15% of its requirement today.

Of course, both China and India have plans to ramp up coal production, but the benefit will accrue over the long term. In any case, not long back, the Chinese government was clamping down on excess production in small mines following many operational accidents.

Conclusion

Overall, the changes indicate that thermal coal prices will stay firm for some time. In this scenario, the obvious beneficiaries in India will be coal/lignite mining companies who can pass on higher prices either for their long-term contracts or sales via e-auctions.

On the other hand, power costs will rise for the average consumer as the government has now invoked a law to force all imported coal-based units to run their plants. With coal being prioritized for the power sector, other energy-intensive industries like cement, textiles, paper, and steel will have to depend on imports leading to higher production costs.

So, how can the government mitigate the impact of this crisis?

While the focus on ramping up renewable energy capacity is welcome, for a developing country like India, coal-based power generation will continue to grow at least for the next decade.

In this regard, the government’s policy to incentivize higher production from captive coal blocks by offering them import parity linked prices is a step in the right direction. Faster regulatory approvals for opening new or expanding existing mines are also important.

On the logistics side, the Indian Railways should take steps to augment its wagon fleet. This adversity can still be a blessing in disguise if the government gets serious about ensuring long-term energy security in the country.

(The author is Chief Investment Officer of Research & Ranking, an equity investment advisory firm)

Disclaimer: The views and recommendations made above are those of the analyst and not of MintGenie.